Stock in Focus – Bollore SE

Jordan Lipson, Portfolio Manager, Cromwell Phoenix Global Opportunities Fund

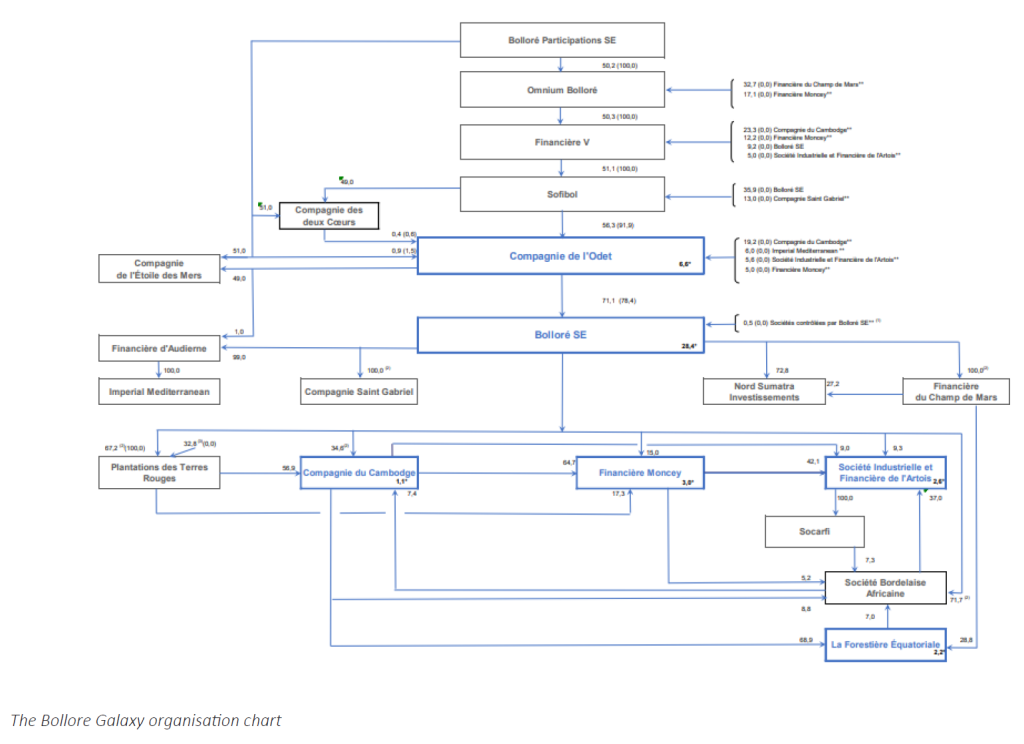

The Bollore Galaxy – An Update

As many readers may be aware, the portfolio has long held an exposure to entities controlled by the Bollore Family. The portfolio’s largest holding is Compagnie de l’Odet (Odet), a French-listed holding company controlled by the Bollore’s. Past generations of Bollore’s were in the business of thin paper manufacturing for uses such as rolling tobacco. In the 1980’s Vincent Bollore was an investment banker. He saw that the old family business was struggling mightily and decided to acquire the distressed business and recapitalise it. Bollore needed to raise external capital to diversify the company’s business interests but wanted to maintain operational control. Like any good investment banker, Bollore achieved this through complex structuring.

The current organisational chart is presented below to demonstrate this complexity, but for the sake of this article there are two key entities, both listed in France. They are:

- Compagnie de l’Odet (Odet)

- Bollore SE

These two companies own meaningful stakes in each other, creating an “ownership loop”. This structure can make the group difficult to analyse at first glance and importantly obscures the true value of the underlying assets.

HPS has unequivocally delivered great results in recent times, with growth driven by demand from data centres as well as other industrial applications. HPS also has a highly professional investor relations function, with detailed quarterly results presentations, slick ESG reporting and analyst coverage by major Canadian investment banks. HPS has been rewarded with a fair valuation. It has a market cap above $1.5 billion1 and trades on a price to earnings ratio above 17x. While HMM’s business hasn’t quite kept pace with HPS’s eye watering growth, over the past seven years it has grown revenues at approximately 10%

HPS has unequivocally delivered great results in recent times, with growth driven by demand from data centres as well as other industrial applications. HPS also has a highly professional investor relations function, with detailed quarterly results presentations, slick ESG reporting and analyst coverage by major Canadian investment banks. HPS has been rewarded with a fair valuation. It has a market cap above $1.5 billion1 and trades on a price to earnings ratio above 17x. While HMM’s business hasn’t quite kept pace with HPS’s eye watering growth, over the past seven years it has grown revenues at approximately 10%