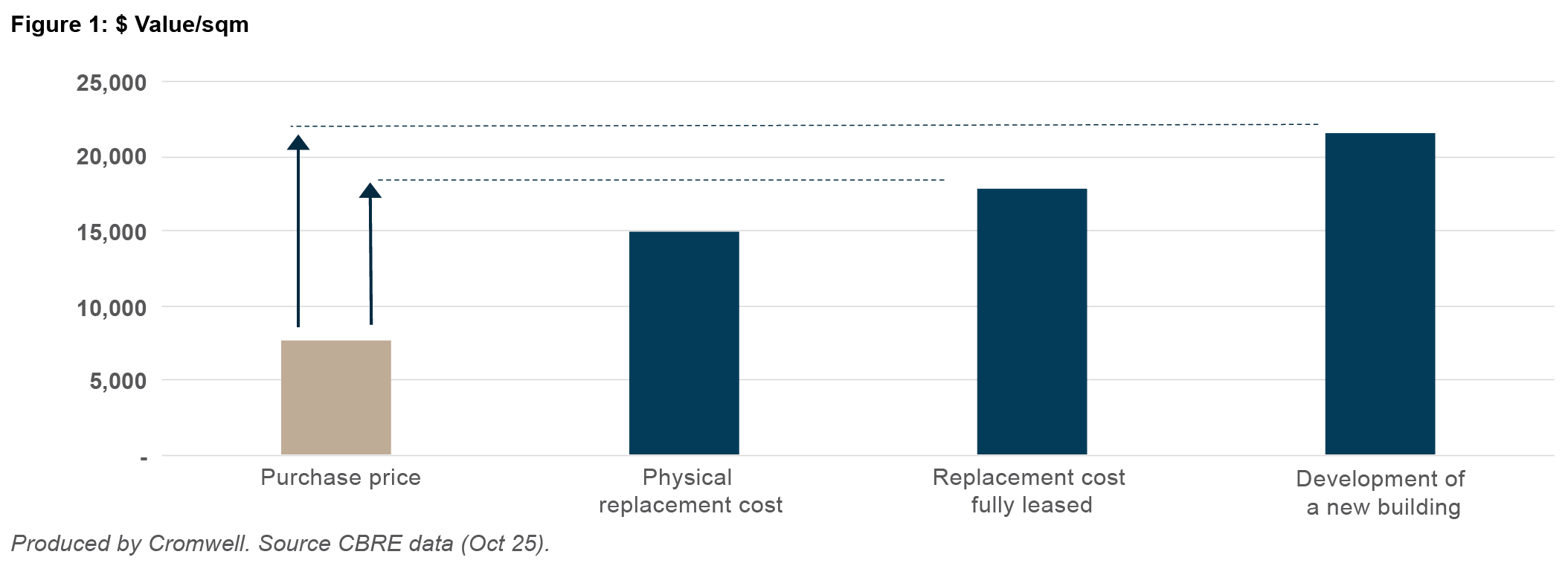

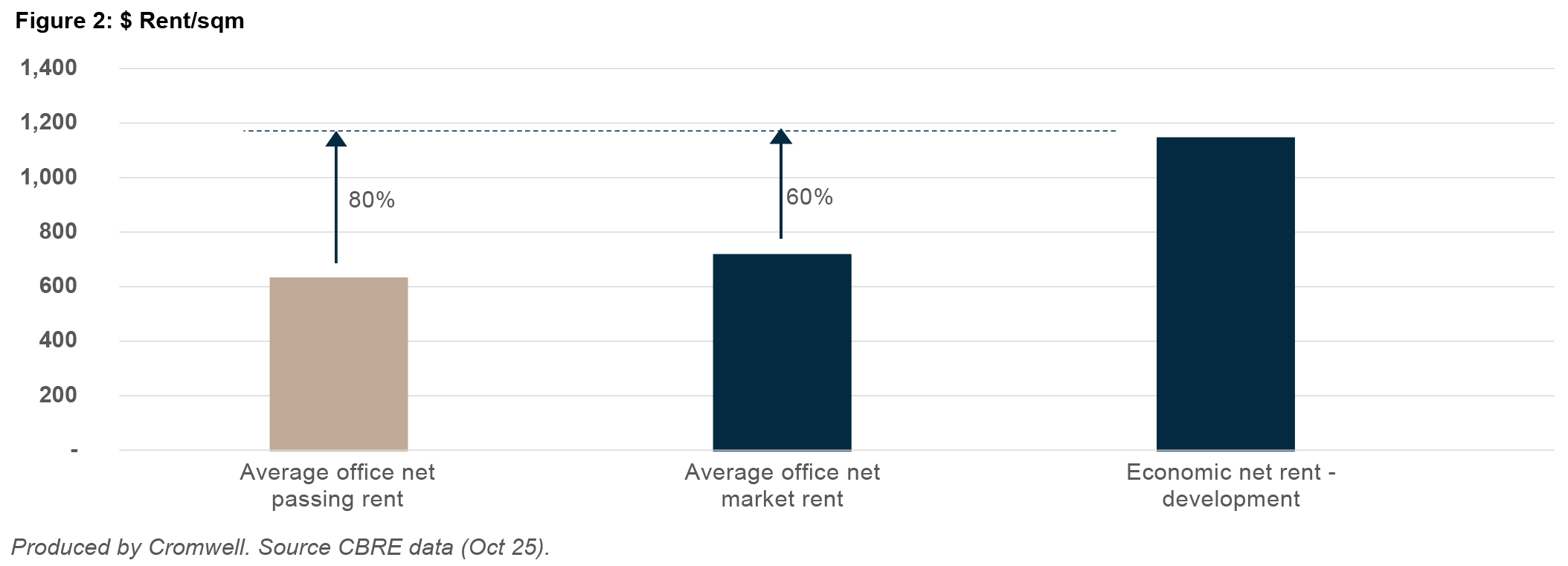

How do we define replacement cost

For the purposes of this analysis, replacement cost is defined as the estimated cost to construct a comparable new office building today, using current materials, labour and building standards, excluding development profit and interest costs.

This definition is deliberate: it isolates the physical cost base of an equivalent building, covering structure, services, façade, fit-out, compliance and professional fees, without embedding commercial assumptions that can vary significantly across developments. This “pure build” framing aligns with industry practice used by CBRE, JLL and Knight Frank when assessing whether the market is pricing existing assets above or below the cost of new supply.

How and why replacement costs have increased

Replacement costs have risen materially across Australia over the past five years, reflecting sustained increases in the cost of delivering new office stock. ABS Producer Price Index data shows non‑residential building construction output prices have risen by around 35% nationally and approximately 40% in Queensland between March 2020 and December 2025.1 This uplift flows directly into replacement cost, as higher material, labour and construction input prices raise the physical cost base required to bring new buildings to market, widening the gap between build‑new economics and the pricing of existing assets.

Fit‑out works represent a significant portion of overall office delivery costs, and market data indicates they have risen more rapidly than base‑build costs since the pandemic. TRS Tenant Representation Services reports that office fit-out costs have increased around 40% since the pandemic, driven by materials inflation, labour shortages and heightened sustainability expectations.2 JLL’s 2025 analysis reinforces this trend, noting a 14.6% year-on-year rise in average fit-out costs as occupiers invest in higher quality, tech enabled and hybrid ready spaces.3

These escalating inputs sit behind a broader feasibility challenge across Australia’s office markets. JLL’s 2025 Fit-Out Cost Guide notes rising material and labour costs are stretching delivery timelines and continuing to elevate project budgets. Knight Frank similarly highlights that higher economic rents and rising construction costs are constraining development pipelines, particularly in CBD markets where the feasibility gap has widened.

In Cromwell’s view, these dynamics provide important context for investors: as the cost to deliver new supply rises, less supply ends up being brought to market. Without new supply, vacancy rates tend to decrease as ongoing population growth drives greater competition amongst tenants for space in existing assets. This creates favourable rent growth conditions for well-located buildings with strong amenity, efficient floorplates, and value-aligned rental levels.