February 26, 2026

Cromwell annouces HY26 results

Cromwell Property Group (ASX:CMW) (Cromwell or the Group) announces its financial results for the half year ended 31 December 2025.

Cromwell Chief Executive Officer, Jonathan Callaghan, said: “This has been a successful half-year for Cromwell, with disciplined execution and solid operational performance across the platform.” Key highlights for the six months to 31 December 2025 include accelerated growth, strengthened financial performance, and continued progress across strategic initiatives.

Key Highlights

- Growth accelerated with the acquisition of an industrial management platform and a 19.9% stake in a $472 million Australian industrial portfolio (the Cromwell Industrial Partnership (‘CIP’)), establishing the foundation for a core pillar of the Group’s growth strategy.

- Group AUM rose 13.2% to $5.0 billion, driven by the industrial platform acquisition and stronger portfolio valuations.

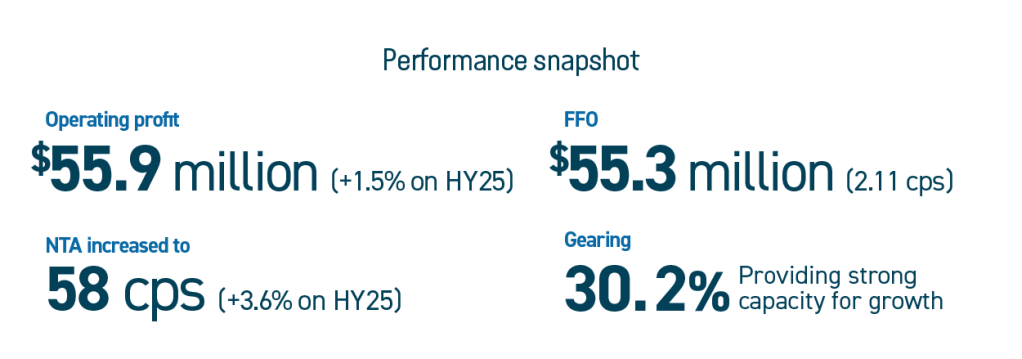

- Operating performance strengthened, with operating profit up 1.5% for the six months ended 31 December 2025.

- The Group’s strong balance sheet provides financial flexibility for growth, with gearing at 30.2%1, significant liquidity of $418 million, and 71%1 of debt hedged, all as at 31 December 2025.

- Investment Portfolio valuations increased by 3.6%1, driven by a successful leasing strategy and high portfolio occupancy of 97.2%1.

- Investment management pipeline continues to build momentum with the Barton1 development progressing on schedule and within budget.

- Distribution guidance of 3.0 cps is reaffirmed for FY26.

We continue to build momentum as we progress our strategy and position the Group to deliver sustainable long-term growth.Jonathan Callaghan, Cromwell Chief Executive Officer

Financial performance

Cromwell reported an increase of 1.5% in operating profit to $55.9 million, supported by the continued strong performance of the Investment Portfolio, which recorded valuation gains of $72.0 million during the period. The Group reported funds from operations (FFO) of $55.3 million, equivalent to 2.11 cents per security, reflecting a payout ratio of 71.0%.

Net Tangible Assets (NTA) increased to $0.58 per security, up from $0.56 per security at 30 June 2025. NTA remains above the current trading price, highlighting the upside potential relative to the Group’s underlying asset base.

Gearing remains low at 30.2%1, providing substantial balance sheet capacity and maintaining significant headroom against debt covenant limits. Cromwell’s $418.0 million of liquidity supports continued flexibility for disciplined capital deployment into growth initiatives.

Investment portfolio performance

Cromwell’s Investment Portfolio delivered a strong performance over the six months to 31 December 2025, with valuations up 3.6% since FY25 to $2.1 billion1, driven by resilient asset fundamentals and improving market conditions. The uplift reflects both sustained leasing activity across key assets and continued stabilisation in valuation metrics as capital markets regain confidence.

Occupancy remains high at 97.2%1, supported by leasing of more than 23,000 square metres during the period. Material uplift was seen at Cromwell’s asset at 400 George Street, Brisbane, where key leases have been extended to 2030 following the exercise of a three‑year lease option by QLD State Government.

Positive market momentum is expected to continue through the remainder of the financial year, supported by firming demand for high‑quality real estate and constrained supply of office space. Together, these factors position the portfolio well for ongoing stable earnings and enhanced returns for investors as the Group continues its growth trajectory.

Strategic growth initiatives

Cromwell advanced its growth strategy during the half through three key initiatives.

Expansion into Australian industrial real estate

Cromwell completed Phase 1 of its transaction with Straits Real Estate Pte Ltd (SRE), acquiring a 19.9% interest in SRE’s industrial portfolio and its management platform, Terre Property Partners (TPP). TPP adds $567 million in AUM, deep industrial expertise and a proven team, strengthening Cromwell’s on-the-ground capability and supporting further growth in investment management.

Phase 2, launching shortly, will bring additional capital partners to the portfolio as it grows through acquisition and development. The existing seven-asset, $472 million logistics portfolio (cap rate 6.1%) provides scale and diversification, with assets in key logistics hubs of Bayswater (VIC) and Salisbury South and Port Adelaide (SA).

New wholesale fund launched

Cromwell launched the Cromwell Creek Street Investment Trust, with a ~$102 million capital raise underway to acquire 100 Creek Street, a 24-level, ~20,000 sqm Brisbane CBD tower. The asset is 94.3% occupied with a diversified tenant base.

The Fund targets an 8.0% p.a. monthly distribution yield, 100% tax-deferred distributions for the first two years, and a 15% target equity IRR over five years. Independent research has rated the Fund “Recommended.”

Barton1 development progressing to plan

Cromwell’s Barton1 development is forecast to complete on schedule and within budget for mid-2027 completion. The 19,800 sqm office building is fully pre-leased to a Commonwealth Government tenant on a 15-year lease, plus a 5-year option, providing long-term income security. Given the challenging development environment, the fixed-price contract, secured pre-lease, and strong tenant covenant position Barton1 as a rare and compelling opportunity.

Investment Management update

Growth in Cromwell’s Investment Management business was driven by the acquisition of TPP and the 19.9% interest in CIP during the period, and the Group now manages $2.8 billion across Australia and New Zealand.

The Cromwell Direct Property Fund (DPF) holds seven2 assets valued at $470.3 million, with the five direct assets valued at $396.5 million, representing a 1.3% valuation increase since at 30 June 2025. Portfolio occupancy remains high and unchanged at 96.4%, with the portfolio’s cap rate tightening to 7.7%.

DPF has commenced the wind up process following the Periodic Liquidity event voted for by investors in late 2025. As part of this process, the sale of 545 Queen Street settled on 19 December 2025, delivering $77 million in net proceeds after selling costs.

Outlook

The Group has made strong initial progress in implementing its strategy to grow third‑party funds under management, broaden our capability set and investor base, and bring to market new products in the office and industrial sectors, with continued work underway in the retail sector, which remains a key focus.

Capital deployment will continue to support growth through both organic initiatives and targeted inorganic opportunities, with an emphasis on strategic, value‑add acquisitions in Australia’s core sectors in partnership with new, aligned capital partners.

Cromwell will maintain strong occupancy across its Investment Portfolio to support income during the current growth phase, underpinned by targeted leasing campaigns, spec‑suite delivery, and capital works designed to enhance occupancy, grow WALE and rental income.

The Group continues to monitor its capital management position by preserving gearing headroom to enable opportunistic transactions, proactively managing refinancing to protect interest costs and liquidity, and maintaining disciplined capital allocation.

The Group reaffirms its expectation of an annual distribution of 3.0 cents per security for the 2026 financial year.

Footnotes:

- Excluding 475 Victoria Ave, Chatswood, which is classified as held for sale and includes Barton1, currently under development.

- DPF assets are comprised of 5 direct assets and 2 assets in underlying unit trusts.

Related articles

Learn

January 22, 2026

Stock in Focus – Young & Co.’s Brewery PLC

Jordan Lipson, Portfolio Manager, Cromwell Phoenix Global Opportunities Fund

Old business in a modern world

Young & Co.’s Brewery PLC (Young’s) has been an investment within the Cromwell Phoenix Global Opportunities Fund since its inception six years ago. Its history goes back far longer than that, with connections to its previously owned brewery dating back to at least the 1500s, but likely longer than that. Today Young’s owns and operates 288 predominantly freehold pubs across the United Kingdom. A combination of cyclical and structural factors have led to extreme pessimism in the UK pub sector, however Young’s is well run, financially sound and trades at a meaningful discount to readily assessable value. Furthermore, the portfolio accesses this opportunity at a further discount, given its unique shareholding structure. This makes Young’s an attractive investment, squarely within the portfolio’s investment universe.

Looking back

Records of the Ram Brewery, based in Wandsworth in Southwest London, date back to 1581, when it was run by Humphrey Langridge. After changing hands and being passed down generations, the brewery was sold to Charles Allen Young and Anthony Bainbridge in 1831, who had supplied brewing equipment to the previous owners of the brewery. It was then inherited by Charles Florance Young in the late 1880’s, at which point Young & Co.’s Brewery Ltd was established. Not long after, in 1898, the business was listed on the London Stock Exchange. The company’s history of pub ownership also goes back centuries, with a Young family partnership acquiring 88 pubs alongside the brewery. This was an early form of what is now known as “vertical integration”, with the pub’s major focus being the sale of beer made by the Ram Brewery.

Young’s and the Young family were titans of the UK beer scene. Those who grew up in London in the 1900s would probably have ordered many a pint of Young’s Original, or Young’s Special. Young’s was run by John Young for much of the late 1900s, until he retired as Chairman in 1999. The brewery was known to be a family business, that deeply cared about its staff, with many generations of family members working at the Wandsworth site. Historically, it is fair to say occupational health and safety standards were traded for a positive work environment, with Ram being the last “wet brewery”, with staff able to have a healthy sampling of the product at work until the 1970s. Ram was the longest continually running brewery in the UK until 2006 when it was decided that it would close its doors. The now valuable property was to be sold off for much needed residential housing. Up until it closed, beer was still delivered by horse to pubs serving Young’s within a two mile radius of the brewery. The iconic site hosted an animal paddock and was visited by both the Queen and the Queen’s mother. John Young passed away in 2006 not long after the decision to close the brewery was finalised. The last batch of beer produced at the site was served at his funeral.

“In this tough environment, Young’s grew like-for-like sales by 5.7% in the previous financial year and has grown that figure by more than inflation for over a decade.”

HPS has unequivocally delivered great results in recent times, with growth driven by demand from data centres as well as other industrial applications. HPS also has a highly professional investor relations function, with detailed quarterly results presentations, slick ESG reporting and analyst coverage by major Canadian investment banks. HPS has been rewarded with a fair valuation. It has a market cap above $1.5 billion1 and trades on a price to earnings ratio above 17x. While HMM’s business hasn’t quite kept pace with HPS’s eye watering growth, over the past seven years it has grown revenues at approximately 10%

HPS has unequivocally delivered great results in recent times, with growth driven by demand from data centres as well as other industrial applications. HPS also has a highly professional investor relations function, with detailed quarterly results presentations, slick ESG reporting and analyst coverage by major Canadian investment banks. HPS has been rewarded with a fair valuation. It has a market cap above $1.5 billion1 and trades on a price to earnings ratio above 17x. While HMM’s business hasn’t quite kept pace with HPS’s eye watering growth, over the past seven years it has grown revenues at approximately 10%

The healthcare and social assistance sector remains an essential and growing industry, accounting for 8% of the Australian economy5 and 16% of employment6. Healthcare property encompasses a range of asset types, from hospitals to medical centres, life science facilities and specialist disability accommodation. While some sub-sectors – such as private hospitals – are facing well publicised issues, we believe medical centres/offices are resilient to these challenges and well placed to benefit from several demand tailwinds. These assets are essential to communities across the country, providing a range of primary and secondary care such as GP, specialist, and allied health services.

The healthcare and social assistance sector remains an essential and growing industry, accounting for 8% of the Australian economy5 and 16% of employment6. Healthcare property encompasses a range of asset types, from hospitals to medical centres, life science facilities and specialist disability accommodation. While some sub-sectors – such as private hospitals – are facing well publicised issues, we believe medical centres/offices are resilient to these challenges and well placed to benefit from several demand tailwinds. These assets are essential to communities across the country, providing a range of primary and secondary care such as GP, specialist, and allied health services. Industrial property has been the top-performing real estate sector over the past decade13, propelled by strong rental growth as demand for space outpaced development of new supply.

Industrial property has been the top-performing real estate sector over the past decade13, propelled by strong rental growth as demand for space outpaced development of new supply. Convenience retail property assets are generally smaller, standalone shopping centres – often anchored by supermarkets – that service the surrounding suburbs by providing convenient access to essential goods and services.

Convenience retail property assets are generally smaller, standalone shopping centres – often anchored by supermarkets – that service the surrounding suburbs by providing convenient access to essential goods and services.