March 2023 quarter ASX A-REIT market update

Stuart Cartledge

Market commentary

The S&P/ASX 300 A-REIT Accumulation Index moved marginally higher in the first quarter of the year – rising 0.3%. This performance can be seen as relatively muted, considering the 10-year Australian Government bond yield dropped 0.5% over the quarter. The broader equity market outperformed property, with the S&P/ASX 300 Accumulation Index adding 3.3%. In February, most companies under coverage reported their half yearly earnings to 31 December 2022.

Valuations were broadly flat across the sector, although the tone was more cautious looking forward. A feature of discussions surrounded the impact of rising interest rates on future earnings and property valuations. Interest rate relief towards the end of the quarter should support earnings and limit downward revisions to valuations.

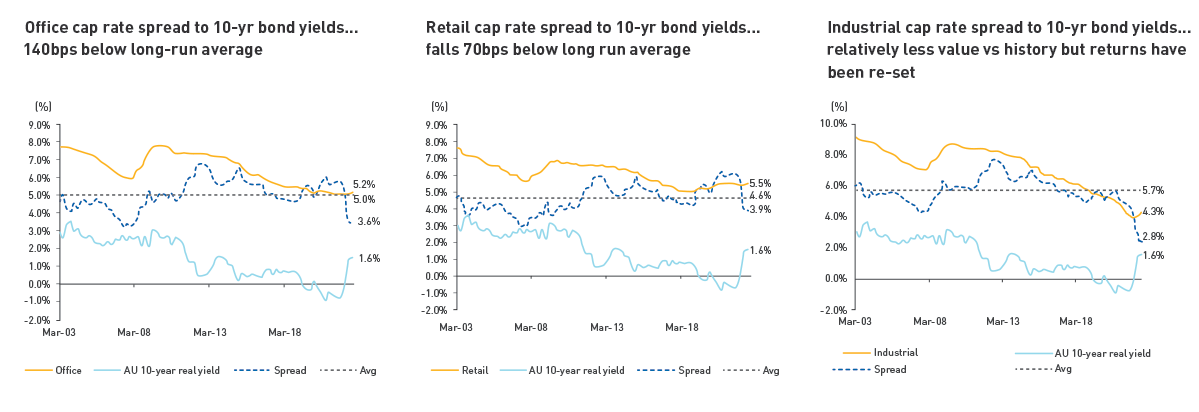

REITs with exposure to office markets were underperformers in the first quarter of the year. Amongst an environment of concern over the future use of office spaces, vacancy and incentives in key markets have remained stubbornly elevated, leading some to have concerns surrounding the sustainability of cash flows coming from office building ownership.

Many listed office owners argue that there will be a bifurcation, by which higher quality offices will endure and lower quality buildings will face a challenging future. Time will tell if this is correct. For the quarter, Cromwell Property Group (CMW) lost 15.1%, while Mirvac Group (MGR) dropped 2.3% and Dexus was off 3.1%. Charter Hall Group’s (CHC) earnings are particularly leveraged to office markets, given its franchise in office funds management. Its share price fell 8.2% during the quarter.

The drop in bond yields and short-term interest rate expectations were supportive of residential property developers during the period. Stockland (SGP) is the largest residential land developer in the country and as such rose 9.6% during the quarter. SGP’s management had previously suggested they would slow down land accumulation in a weakening market. At its half yearly report, the tone changed, with a goal to add to its land bank, supported by a new joint venture with Japanese real estate developer Mitsubishi Estates.

Smaller capitalisation residential developers AV Jennings Limited (AVJ) and Peet Limited (PPC) also outperformed, gaining 4.0% and 3.1% respectively. Owners of large shopping centres reported resilient financial results to 31 December, with specialty sales and rental outcomes broadly above expectations. Vicinity Centres (VCX) upgraded its full year earnings guidance, supported by almost flat re-leasing spreads, improving from -6.8% at the same time a year ago. VCX finished the quarter up 0.1%. Scentre Group (SCG) released earnings guidance for calendar year 2023, which was higher than expectations. It finished the quarter down 1.6% with some fearing a weaker economy moving forward.

Offshore, Unibail-Rodamco-Westfield (URW) outperformed on the back of results that are best summarised as less bad than expected. For the quarter it rose 3.6%. Industrial property owners faced a mixed period. In terms of property valuations, capitalisation rates increased sharply, however valuations were mostly slightly higher, supported by an acceleration in market rents around the nation’s industrial leasing markets. Industrial fund manager Goodman Group (GMG) led the way, adding 8.2%, while Growthpoint Properties Australia (GOZ) lifted 2.0% and Centuria Industrial REIT (CIP) gave up 2.6%.

Market Outlook

February’s reporting season showed a property sector that was mostly performing solidly from an operational perspective. Increased interest rates are however unmistakably a drag to earnings, given the use of debt across real estate investment trusts. Current gearing levels are however very manageable. Property valuations to 31 December 2022 mostly showed slightly negative revaluations.

The industrial sub-sector continues to be the most sought after, given the tailwinds of e-commerce growth, the potential onshoring of key manufacturing categories and the decision by many corporates to build some redundancy into supply chains to cope with current disruptions. All of these factors will support ongoing demand for industrial space, which is evident by rapidly accelerating market rents for properties.

The jury is still out on exactly how tenants will use office space moving forward, but demand for good quality well located space remains. Transactional activity of office assets continues to provide some evidence of value, but transaction volumes have recently reduced. Incentives on new leases do remain elevated and some vacancy in the market is becoming apparent.

We remain cognisant of the structural changes occurring in the retail sector with the growing penetration of online sales and the greater importance of experiential offering inside malls. Recent performance of shopping centre owners has however been strong, with consumers showing resilience. It is interesting to note the juxtaposition of very high retail sales figures despite very low levels of consumer confidence, no doubt impacted by rising costs of living.

The recent increase in bond yields does present a headwind for all financial assets, and particularly yield based sectors such as property. However, with key large capitalisation REITs now trading at a significant discount to the value of their underlying assets and with no value ascribed to embedded active businesses, we believe the sector offers value, particularly in comparison to unlisted property.

Phoenix has for some time discussed the risk of inflation, given the enormous fiscal stimulus and extreme monetary policy setting that we have lived through. In recent times, commentators and bond markets have begun to react to the presence of such a risk. In this environment, long leases with fixed rent bumps, which were previously in high demand, may become relatively less attractive. Historically, real assets such as property and infrastructure have performed well during inflationary periods.

About Stuart Cartledge

About Stuart Cartledge