Five reasons unlisted commercial property is an attractive allocation in uncertain times

In this era of heightened geopolitical and macroeconomic uncertainty, portfolio construction increasingly favours assets capable of delivering durable income, capital preservation, and differentiated return drivers. Unlisted Australian commercial property continues to demonstrate qualities that may support these characteristics.

The immediate backdrop is hard to ignore. On 12 March 2026, the International Energy Agency said the war in the Middle East was creating the largest supply disruption in the history of the global oil market1. At the same time, the IMF has warned that financial stability risks have increased as trade and policy uncertainty remain elevated.

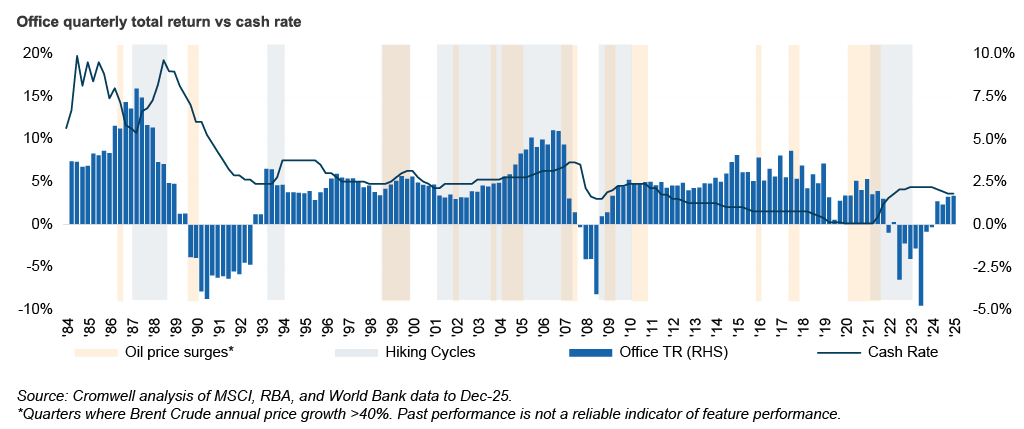

A fractured landscape demands decision-makers weigh risk and resilience more heavily than a decade ago. This note highlights some of the reasons why an allocation to unlisted Australian commercial property is important in today’s uncertain environment, offering attractive returns underpinned primarily by space market fundamentals rather than daily swings in sentiment.