HomeUnitholders approve Term Extension for Cromwell Property Trust 12

November 27, 2025

Unitholders approve Term Extension for Cromwell Property Trust 12

Unitholders in Cromwell Property Trust 12 (C12) have voted overwhelmingly in favour of extending the term of the Trust for a further two years, until 31 December 2027. The resolution was passed at an Extraordinary General Meeting on 31 October 2025, following Cromwell Funds Management’s (CFM) recommendation to wait for market conditions to improve before commencing a sale process. CFM noted that current market conditions are unlikely to support a favourable sale outcome and that an extension would provide flexibility in determining the timing of a future sale.

Strong support for extension

The resolution passed with a clear majority:

Votes FOR the motion: 36,055,173 units (88.57% of votes cast; 57.38% of eligible units)

Votes AGAINST the motion: 4,654,486 units (11.43% of votes cast; 7.41% of eligible units)

Total votes cast: 40,709,659 units (64.79% of eligible units)

Background to the Trust

Launched in 2013, C12 was established to provide monthly income from high-quality commercial property assets. Over its life, the Trust has delivered consistent returns, including notable one-off distributions following asset sales:

5 cent distribution in 2015 after the sale of 10–16 Dorcas Street, South Melbourne

84 cent special distribution in 2020 following the sale of the Rand Distribution Centre in South Australia

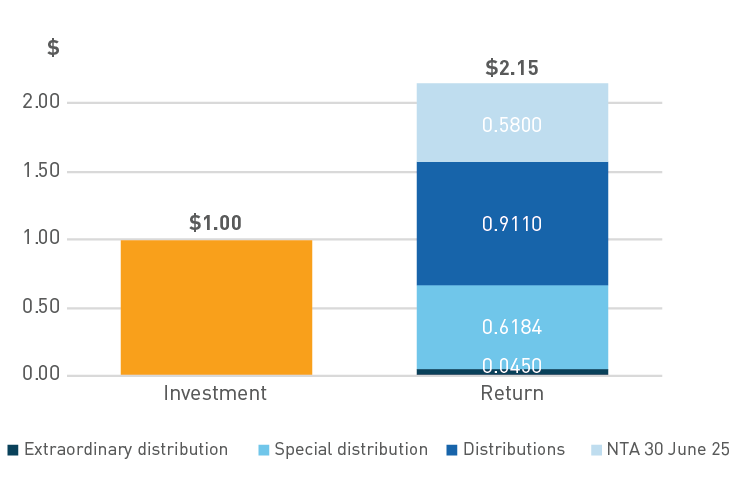

Regular distributions began at 7.75 cents per unit and increased to 9.25 cents by FY2021. At the start of the second term in July 2021, the rate was reset to 5.75 cents per unit, rising to 6.50 cents by FY2025. To 30 June 2025, C12 delivered a notional equity internal rate of return of 11.8% per annum. Every $1 invested in July 2013 has returned $1.57 in distributions and holds a current value of $0.58, equating to a total value of $2.15.

Investment return per $1 invested

C12’s distribution rate will adjust from 6.50 cents per unit per annum to 6.00 cents per unit per annum from November 2025. This change reflects the extension of an interest rate cap that remains beneficial but now carries a higher base rate. Details of this adjustment, along with the potential impact on unit price, were included in the information provided to unitholders ahead of the vote.

Why extend now? Market conditions explained

Cromwell’s Chief Investment Officer, Rob Percy, outlined the rationale for the extension at the EGM. While some indicators suggest office values nationally are stabilising, Melbourne’s market, particularly the CBD and surrounding sub-markets continues to underperform relative to other capital cities.

Key challenges

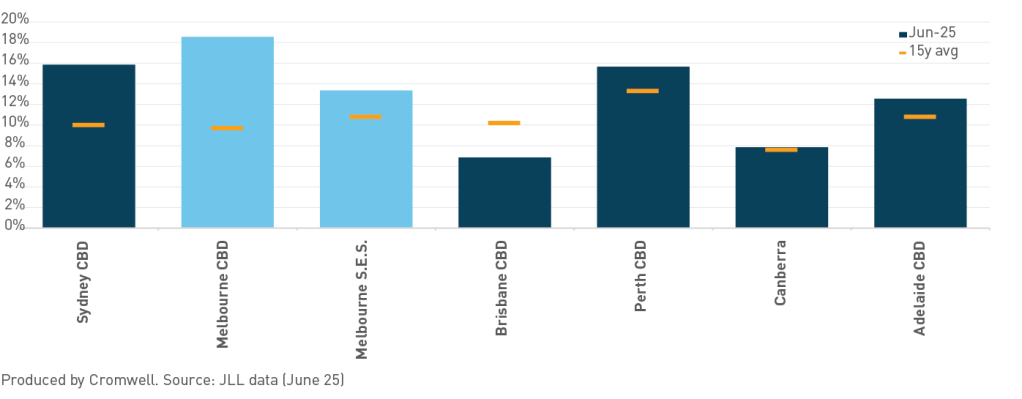

The Trust’s sole asset is in Dandenong, part of Melbourne’s South-East Suburbs sub-market, which accounts for only 2% of the city’s total office space. Market sentiment for the property is influenced by broader Melbourne conditions, particularly the CBD, which currently has the highest vacancy rate among major cities and has underperformed long-term averages.

Prime office vacancy rate

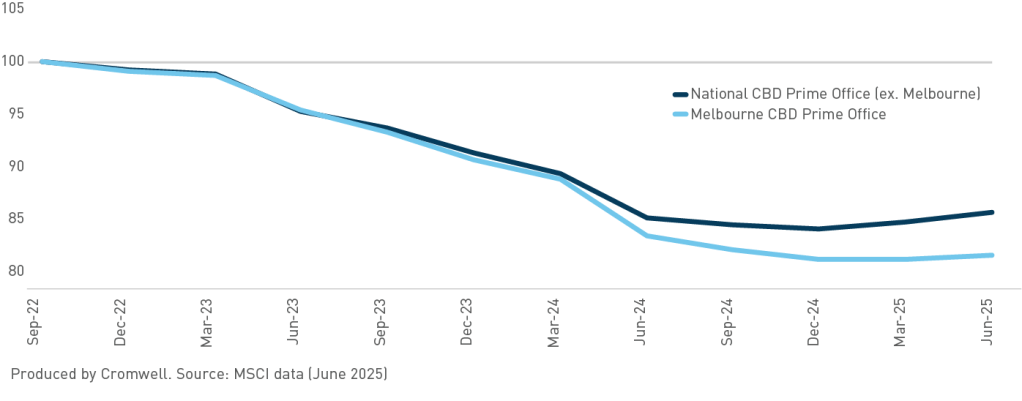

MSCI data, which tracks commercial property performance across Australia, confirms that Melbourne office asset values have underperformed compared to other cities, which recorded increases in asset values during the March and June 2025 quarters.

Office asset value index

Compounding this, national office transaction volumes remain low, and Melbourne’s share of those volumes is significantly below its long-term average. This lack of activity means fewer potential buyers and limited competitive tension.

Office transaction volume

These factors mean a sale now would likely be at a discount to the latest independent valuation.

Despite current challenges, Cromwell highlighted several positive indicators:

Net leasing demand in Melbourne’s prime office market has increased since 2019.

Very low levels of new commercial construction forecast over the next five years may help absorb existing vacancy and support rental growth.

Stabilising yields across sectors are contributing to more stable asset pricing, which could attract more market participants and increase transaction volumes.

The spread between Melbourne CBD prime office yields and the 10-year government bond yield is wider than historical averages, suggesting relative value and potential for recovery.

Real estate pricing is cyclical, and Cromwell believes the market is approaching a turning point. Extending the Trust’s term provides flexibility to capitalise on these improving conditions.

Conclusion

The decision to extend the term of Cromwell Property Trust 12 reflects a considered approach to current market dynamics. By allowing additional time before commencing a sale process, the Trust remains positioned to respond to changing conditions and pursue a strategy aimed at achieving the best possible outcome for unitholders. Cromwell will continue to monitor market developments and provide updates as the extended term progresses.

Related posts

September 2025 direct property market update

Political uncertainty in the US was a defining theme over the last quarter, and it reached a head on 1 October 2025 as funding lapsed and the Federal …

Understanding the property cycle can be useful for investors as it enables them to make informed investment decisions and stay focused on their long-t…