The UMG conundrum

Music has proven to have universal appeal (excuse the pun) across all ages and regions. UMG is the world’s largest music publishing business, having represented 9 of the top 10 artists globally across each of the past three years, including Taylor Swift and Lady Gaga. For readers of a different generation, UMG also owns timeless assets such as rights over The Beatles back catalogue. UMG can be thought of as a toll booth on music consumption.

Since its separate listing in 2021, UMG has typically traded at a premium valuation, given the high-quality nature of its business. Very recently, concern has grown that artificial intelligence (AI) may threaten the quality of this business, both by enabling solo artists to self-publish and by allowing AI to create the music itself. This threat has caused UMG’s share price to drop from a high of almost 29 EUR per share to lows of approximately 15.50 EUR per share. According to S&P CapitalIQ consensus estimates, UMG trades at a 2026 Price to Earnings ratio less than of 16x, which compares to the S&P 500’s price to earnings ratio of just under 26x.

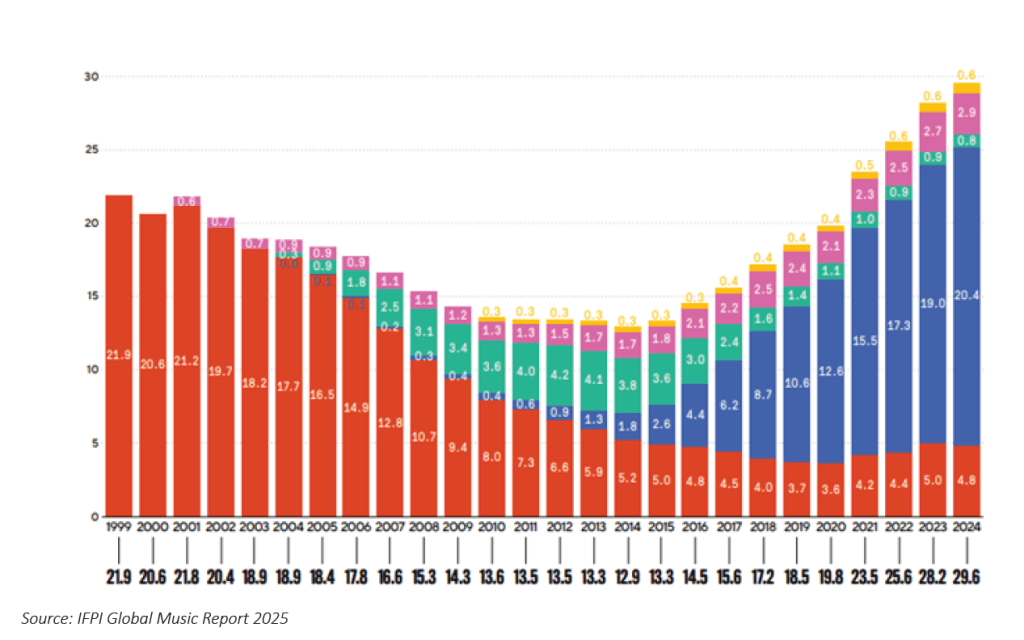

The quality of the music business has been tested before. Physical sales of music, mostly CDs, peaked in 1999. The proliferation of music piracy meant that it took until 2021 for music sales to reach that absolute level again (see below). Adjusted for inflation, music sales are still below that 1999 level.

Streaming services, and their global appeal completely changed the game for musicians and publishers. UMG’s more bullish investors would say that these streaming services have pricing power beyond what they currently charge and are also supported by the tailwind of a growing global middle class that can afford these services. If this is true it would likely mean robust earnings growth for the company for many years to come. UMG’s detractors would say AI developments will take power away from music publishers and extreme believers in AI would say it takes relevance away from the skill and creativity of musicians and songwriters.

Should concerns turn out to be overblown and UMG once again trades at its previous highs, Odet’s NAV would expand to a ~370% premium to its current share price! Alternatively, even assigning zero value to UMG leaves Odet’s NAV at a ~65% premium to the prevailing share price, showing the high margin of safety inherent in this investment. While there are legitimate debates about the future of music, we believe the long-term appeal of professionally produced content remains strong. However, an investment in Odet could still be an excellent investment, even if that belief proves to be optimistic.

The Longer Game

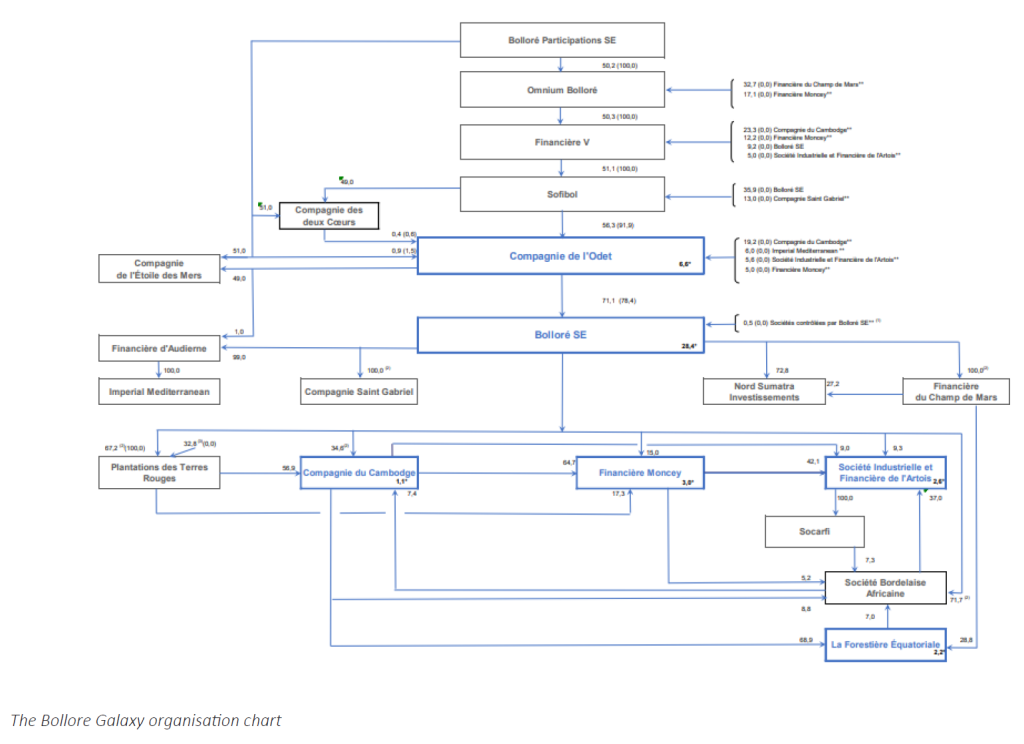

The ultimate result for investors would be a return to glory for UMG, alongside a return of capital from Odet. In recent times, the number of boxes in the organisational chart above has reduced as some simplification has occurred. The Bollore Family has also tried to remove more entities from that chart, yet faced resistance from minority shareholders. Odet itself has bought more and more Bollore shares. This activity (which effectively amounts to a buyback) has accelerated since the entities released their full year results. Most importantly, the recently announced special dividend shows a willingness to return capital to external shareholders and also moves cash around the different entities within the Bollore Galaxy. This may be tactical and act as a prelude to Vincent Bollore’s next move. Possibilities are the basis of much speculation amongst shareholders, but only the Bollore’s know the true endgame. In the short term the distribution allows shareholders to receive a meaningful portion of the NAV back at 100 cents on the dollar. Not a bad outcome for now.