Political uncertainty in the US was a defining theme over the last quarter, and it came to a head on October 1st as funding lapsed and the Federal government shut down, fuelling uncertainty over fiscal discipline and delaying key economic data releases. The shutdown became the longest in history, ending on November 12th after 43 days of disruption. As expected, the episode had limited impact on Australia.

Back home, a number of data prints indicated inflation and growth are both running a touch hotter than expected. The September quarterly CPI increased to 3.2% on a 12-month basis1, rising above the upper bound of the RBA’s target band. While the result was skewed higher by some volatile items like fuel, and administered prices such as utilities and property rates, the breadth of categories running above 3.5% year-on-year suggests some inflationary pressures remain in the domestic economy.

While households’ financial position has been improving, rising cautiousness and a greater degree of saving (rather than spending) threatened to dampen Australia’s economic growth recovery. Those concerns were somewhat allayed by the latest print of the Westpac-Melbourne Institute Consumer Sentiment index which surged by +12.8% to 103.8, marking the first time it has sat in positive territory since early 20222.

Similarly, the unemployment rate fell from 4.5% to 4.3% in October, unwinding the increase seen in the previous month. The result was underpinned by the creation of 55,300 full-time jobs and an unchanged participation rate3. The RBA would have likely welcomed the outcome, which helps avoid the tension that would come with a deteriorating labour market at a time of sticky inflation.

Following the latest data releases, markets now believe the RBA’s easing cycle has concluded, with no further cuts priced in over the forecast horizon4. Economists largely agree, however some forecasters still expect a rate cut in the first half of 2026.

Taken together, economic data suggests Australia is on track and in a better position than most countries. The key question is whether the RBA will leave monetary policy settings in restrictive territory for too long, however the Board is cognisant of the risk and will be guided by the data.

The office sector’s gradual recovery continued, with net demand for space expanding by nearly 57,000 square metres (sqm) over the quarter. Sydney CBD again saw the biggest absolute increase in demand (36,000 sqm), while the 25,000 sqm of net absorption recorded in Brisbane CBD represented the strongest growth on a percentage basis. Sydney’s demand was led by prime stock and the Western Corridor, a precinct which struggled through the pandemic but is now attracting tenants centralising from other markets (particularly north of the bridge). Brisbane’s strong quarter was more broad-based, with occupied stock increasing across the quality spectrum. Occupied space contracted in Canberra, the worst performing market over the quarter, largely due to the consolidation of a federal government department.

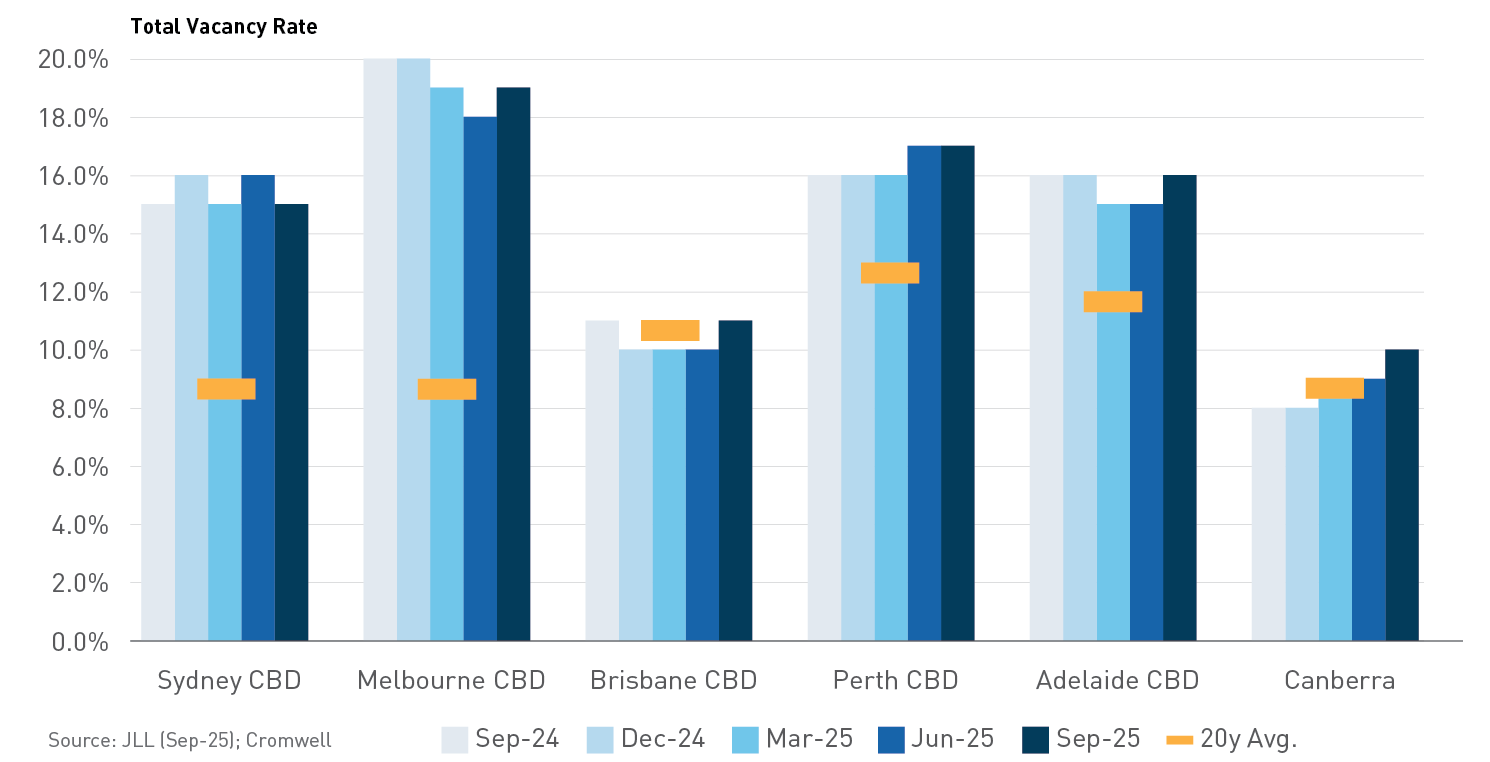

Despite the positive demand result, the national CBD vacancy rate edged +0.1% higher to 15.1% due to weakening conditions in lower quality stock. Sydney was the only CBD market to record a decrease in vacancy rate, underpinned by the absence of development completions over the quarter. Four projects were brought to market in Melbourne CBD and pushed the vacancy rate up +0.4%, however it remains below the peak seen in December 2024. Adelaide saw the largest increase in vacancy as 50 Franklin St reached completion with space still unleased.

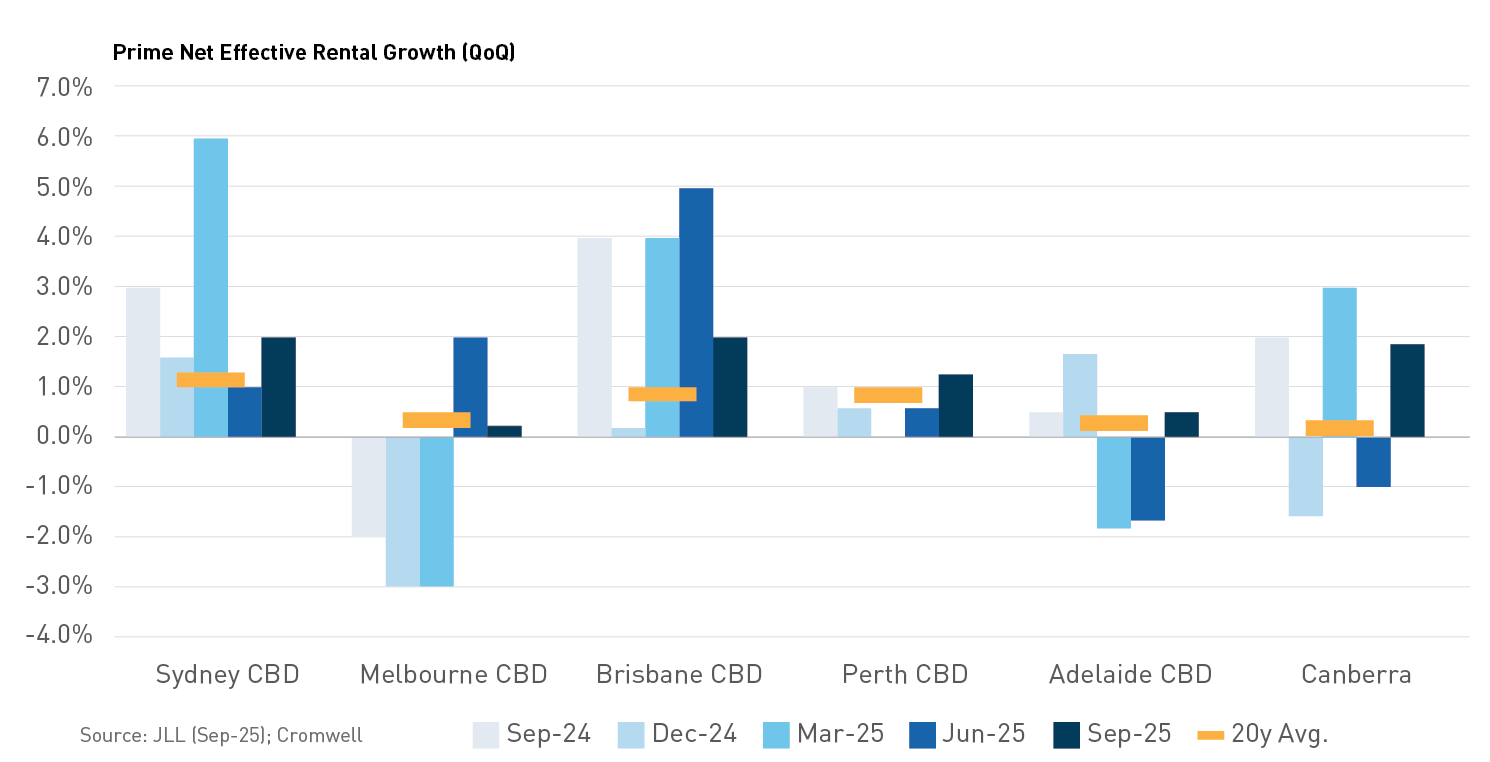

National CBD prime net face rent growth maintained its strong pace, increasing +1.2% over the quarter and +5.9% over the 12 months to September. Canberra recorded the strongest growth over the quarter despite its softening vacancy rate – there is significant variance in this market as tenants prioritise higher quality premises with strong ESG credentials in specific precincts. Growth in Brisbane CBD also continued at pace, reflecting favourable leasing conditions. Prime incentives increased slightly in Canberra, consistent with the shift to newly developed premises, but remained relatively unchanged across the other markets. The combination of solid face rent growth and stable incentives contributed to higher rents on an effective (incentive-adjusted) basis. This was the first quarter since June 2022 where net effective rents increased in all the major CBD markets.

Office transaction volume strengthened over the quarter to $1.3 billion, but this level remains below the long-term average. The biggest recovery was recorded in Melbourne, which was the top-performing market (by dollar volume) for the first time since September 2022. Similar to last quarter, a lack of large deals dampened the national volume figure. There was further evidence that the office valuation cycle is at, or close to, the bottom, with average prime yields unchanged in every CBD market.

The ABS ceased publication of the Retail Trade series after the June release. While this reduces the granularity of retail data available, the Household Spending Indicator series still provides a solid read on consumer activity. Supportive conditions maintained the pace of spending growth over the quarter. Groceries continued to record stronger growth than discretionary categories, such as Clothing, while the mining states of Western Australia and Queensland continued to outperform New South Wales and Victoria.

Supply remains very constrained, particularly at the “big end of town”. There was no Regional shopping centre stock added for the fifth consecutive quarter, while a single Sub-Regional centre reached completion. Development of Neighbourhood centres is more pronounced, with annual stock growth running at 1.3% as at September. However, this is consistent with the delivery of new centres in population growth corridors and is still less than half the rate of growth averaged over the last 20 years.

This lack of supply is contributing to solid rent growth. On a net basis, Regional rents have grown 0.9% over the past year, outpacing Sub-Regionals and Neighbourhoods. Similar to office, Sydney and South-East Queensland recorded the strongest retail rent growth over the quarter.

It was another solid quarter of retail transaction activity with dollar volume totalling over $2.1 billion. The result was underpinned by Regional centres, as partial stakes in Bankstown Central and Westfield Chermside changed hands. Large Format activity was also elevated, headlined by the portfolio sale of six Bunnings assets by Wesfarmers. Neighbourhood centres saw slightly less activity than normal, while no Sub-Regional or CBD assets transacted. There was a moderate level of yield compression recorded over the quarter, led by Sydney which is typically the bellwether market for capital. Neighbourhoods tightened the most nationally, as investors continue to be attracted to convenience assets aligned to non-discretionary spending. Perth was the only market where yields were unchanged across every core shopping centre type.

Occupier take-up (gross demand) was largely in line with last quarter, totalling just over 823,000 sqm. Demand for this quarter was less dominated by a single tenant movement, with the largest leasing deal comprising just over 36,000 sqm of space. Transport & Warehousing was the main driver of the result with over 300,000 sqm of gross demand recorded, while a pickup in Manufacturing leasing helped offset weaker demand from Retail & Wholesale Trade. On a geographical basis, the result was largely consistent with last quarter – Sydney the most active market followed by Melbourne and Queensland.

Rent growth improved slightly on last quarter, averaging +0.8% nationally over the three months to September. Sydney was the top-performing market, with its Inner West precinct recording the strongest growth nationally (+3.5%) and the Outer Central West precinct also recording robust quarterly growth of +2.0%. Adelaide saw strong growth across its southern precincts and remains the top-performing market on an annual basis. Prime incentives increased in every Melbourne precinct, dragging effective rents lower, but were largely unchanged across the rest of the markets.

Delivery of new supply almost halved compared to last quarter, with less than 414,000 sqm of space brought to market nationally. This was the lowest quarter of supply since March 2023 and the most muted 3rd quarter since 2021, with limited completions in Brisbane and a lack of large projects the key drivers. Sydney and Melbourne accounted for 79% of supply over the quarter, a greater proportion than is typical. There is currently nearly 750,000 sqm of space under construction and due to complete in 2025, however, actual delivery may slip into subsequent periods given construction delays are persisting.

Industrial transaction volume strengthened further over the quarter, totalling nearly $3.5 billion across 102 deals. This was the highest number of deals conducted in a quarter since the data series commenced. Sydney and Brisbane were the standout markets, accounting for 60% of dollar transaction volume. The largest transaction of the quarter was Goodman’s acquisition of a 196-hectare site near the under-construction Western Sydney International Airport for around $575 million. While capital continues to prioritise Sydney, Perth was the market which saw the largest compression in yields (-25bps in every submarket). Brisbane also continues to be viewed favourably, with yields compressing in every submarket by 13-20 basis points.

Sign up to Insight Magazine

Stay informed about investing strategies, finance news, property market updates, and more by signing up for Insight. Build a solid foundation of investment knowledge to help you make the right investment decisions and guide you in planning your investment journey.

Trade policy uncertainty remains a headwind for investor confidence. While the global economy is gradually adapting to the current tariff settings, lower courts have ruled the measures illegal. The Supreme Court is set to hear the case from 5th November, with a final ruling likely in early 2026. If the Court upholds the lower-court decisions, the Trump Administration is expected to explore alternative legal avenues to re-establish the tariffs. In practice, the near-term economic impact may be limited, but the ongoing legal and policy uncertainty is likely to keep risk sentiment cautious until the issue is resolved.

Australia is somewhat insulated from the impacts of global volatility, including the most recent tit-for-tat escalations between the US and China. The key considerations domestically are the trajectory of services inflation and the willingness of the RBA to step in and stimulate activity if the labour market deteriorates more quickly. The economy is beginning to transition from public-led growth to private sector investment, but a more supportive monetary environment may be required to maintain momentum.

The commercial property market continues to stabilise, with improving sentiment evident in both capital flows and leasing fundamentals. Construction remains prohibitively expensive in most circumstances, cramping development pipelines and supporting the outlook for existing assets. Office appears to have reached an inflection point, while retail and industrial pricing continues to firm. As confidence returns to the asset class and institutional capital re-engages, identifying compelling opportunities will increasingly depend on a deep understanding of asset quality and positioning.

Footnotes

Cromwell analysis of ABS data (Nov-25)

Westpac-Melbourne Institute (Nov-25)

ABS (Nov-25)

ASX (Nov-25)

Related posts

December 2024 quarter ASX A-REIT market update

The S&P/ASX 300 A-REIT Accumulation Index gave back some of the gains seen in the previous quarter, dropping 6.1%. Property stocks underperformed …