Industrial: Still delivering the goods

Colin Mackay, Research & Investment Strategy Manager, Cromwell Property Group

Industrial has been Australian real estate’s star performer for a decade, notching up an annualised 10-year return of 14.2%1. While the rate of new supply has increased, the availability of space has been unable to match pace with surging demand. Australia has become the lowest vacancy industrial market in the world2, contributing to record rental growth of almost 25% in the year to March 20233. The sector’s strong momentum continues, and the outlook is bright, as several long-term tailwinds drive demand.

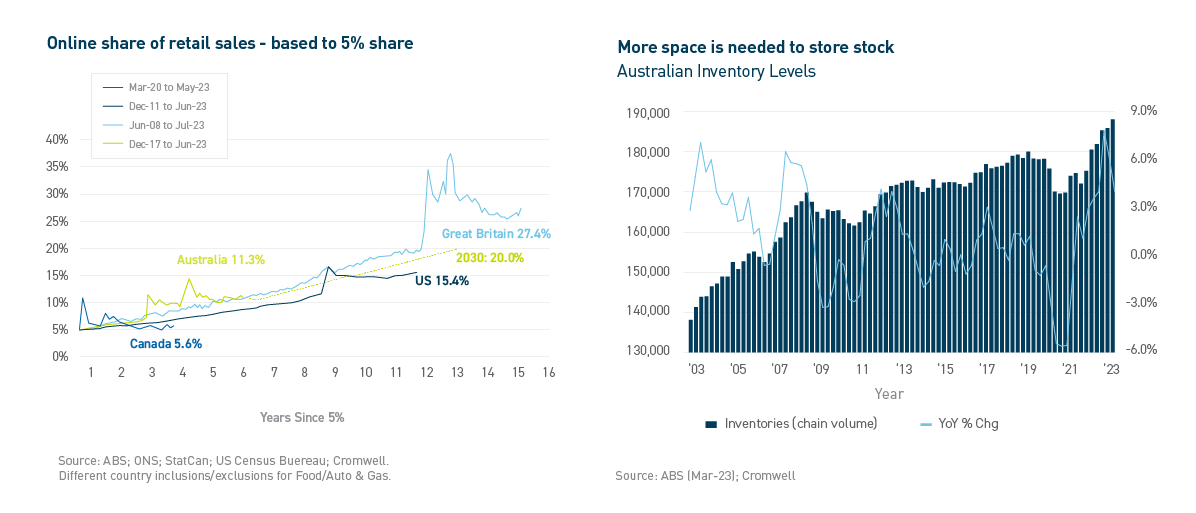

E-commerce

The shift in retail activity from physical stores to digital channels drives demand for industrial space in several ways:

- warehouse space is needed to store inventory which would have otherwise sat in a store;

- e-commerce tends to offer a wider range of products, rather than the curated selection that a specific retail store might be limited to, necessitating more storage space; and

- goods purchased online have higher rates of return, and space is needed to handle the reverse logistics.

Increased storage and space needs mean pure-play e-commerce requires three times the distribution space of traditional retail4. Customer preferences are primarily driving the shift to online, particularly as demographic change sees ‘digital natives’ become the dominant consumer segment. As scale and investment lead to greater efficiencies and profitability, the shift may gain another momentum boost.

E-commerce in Australia is following a similar trajectory to Great Britain – it is on track to hit a market share of 20% of all retail sales by 2030 despite growth slowing from pandemic peaks. With 70,000sqm of logistics space needed for every incremental $1 billion of online sales5, e-commerce alone could generate industrial space demand of almost 600,000sqm p.a. over the next seven years6.